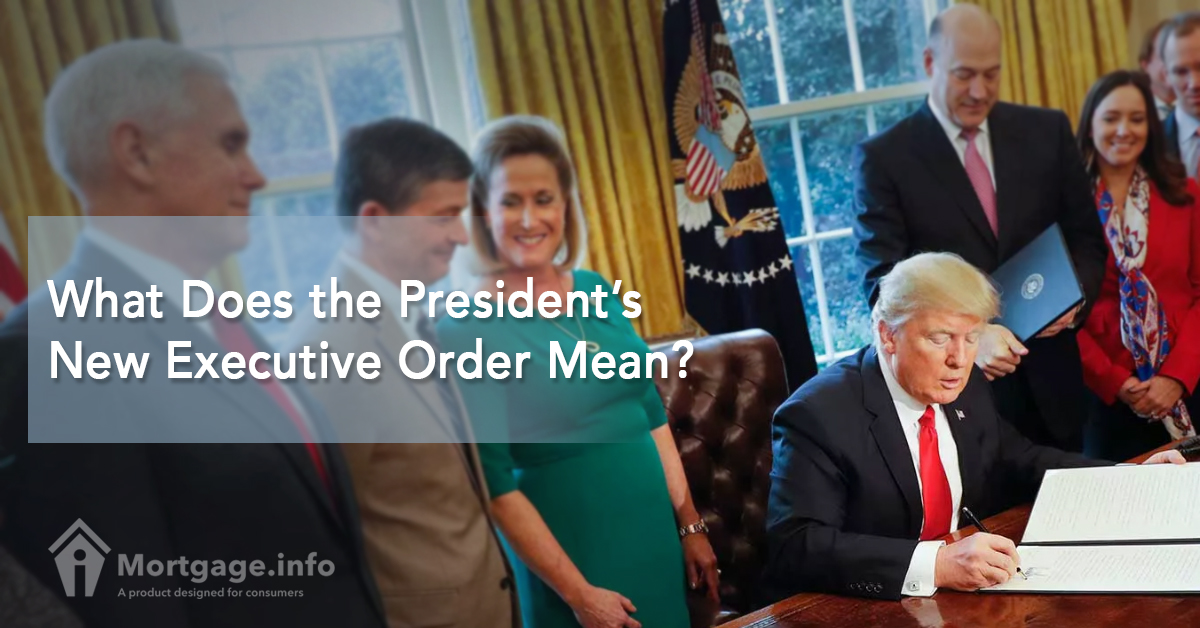

On Friday afternoon, February 24, with a number of America’s top businessmen on his back, President Donald Trump signed an executive order that commands all federal agencies of the country to form core task forces. These task forces are to be assigned to examine the laws and regulations of their assigned agencies and see which of these rules should be kept, junked, or changed to fit with the ruling party’s agenda.

With the top executives of major US corporations Dow Chemical Co (DOW.N), Lockheed Martin Corp (LMT.N) and U.S. Steel Corp (X.N), Pres. Trump requires that the said order should take effect within 60 days, with progress reports to be made within 90 days.

So what does this mean for the average American like you and me?

The ruling Republican party is posed to cut 75 percent of the regulations and laws that they think are hindering Americans from getting their jobs, and companies from creating these jobs.

The existence of current regulations and laws, they claim, are stopping many eligible Americans from getting the jobs they need, and the companies from exercising their business interests.

Petty politicking

Many are saying the conservatives are fixed at undoing what the previous administration has cost billions of dollars and many years to establish, although the Obama administration says that the cost of putting up these initiatives were outweighed by the benefits that they serve.

The new administration thinks too many of these regulations are “repetitive” and “horrible.” The president says that every regulation should only have to go through a simple test: if it makes life better or safer for American workers and consumers.

Why do we need regulations anyway?

Regulations are set for a reason. First, to make sure a certain privilege is fair to everyone. Take for example, the privilege of homebuyers to get a mortgage from the USDA.

USDA loans are designed to cater to low-to-moderate income borrowers. Therefore, high-tier borrowers have lesser chance of accessing the privileges that might otherwise be so easy for them to qualify should there be no regulation in one important aspect: income requirements.

The regulation on income requirement sifts through applicants who have low-to-moderate income profiles because they are the ones who are in most need of these loans. High-income borrowers can easily acquire mortgage programs through conventional lenders. If you take out this simple regulation, there would be no filter as to who gets the loan. And given that the lenders are only interested in their own profits, there would be no loans available to the people who earn less.

The same rule applies among companies who are competing in the market. Without regulations, there is a high possibility that a major company would monopolize business and form a single, large empire who will have control over a region’s economics.

In a free world, a single, all-encompassing entity holding both your opportunities and privileges is a threat to your very liberty.

Regulations also help prevent incidences of fraud and deceit which, even within the strict existent laws today, many determined fraudsters still succeed to exploit.

When it’s about safety

Another important reason why regulations (and even tight regulations) should exist is the safety of workers. Unwanted circumstances can happen anytime and many of these are prevented by proactive, strict trade and occupational regulations.

It is not enough, for example, to hire electrical contractors with only home and basic training, for a job that requires extensive field knowledge and massive machinery experience. Regulations exist to make sure the job is fit for the man. Failure in this area could result to a waste in employer investment, and a huge risk to the health and safety of the poorly-selected employee.

These examples are pretty basic but gives you an idea why rules and regulations, though a bit of a headache in the path to job qualification, should be kept in place.

How does it affect companies?

Not only does the order apply to workers but most importantly, to large corporations who might be having trouble with current strict laws. Take for instance, financing.

Investors need money to keep their business running. Sometimes they have the needed money at hand, but most of the time, they depend on investors and financing.

To get financing or what might be better termed as loans, these corporations need to jump through hoops in order to get the hefty sum of money they need. Financial regulations in place make sure only the most capable borrowers are able to borrow money for their business.

Click here to get matched with a lender>>

This poses problems to not just large corporations but also to small time business owners. Tight regulations could isolate so many small business potentials and discourage inventors and idea makers from pursuing their ingenious intentions.

So in your thinking, would the president’s plan to cut 75 percent of regulations be a good idea?

This concerns not just workers and companies but also you as a homeowner.

The Dodd-Frank Act, for example, which prevents lending companies from taking advantage of financially-vulnerable borrowers, has received a reform orderfrom the president last month. Slacking on lending regulations could cause another housing disaster – which caused the 2008 crisis – to happen again.

A reform in housing regulations could help ease or tighten your access to credit and financing. Which is which, no one could be sure as of now as the impact of the order remains to be seen. Either way, you should brace yourself for more law shifts. Indeed, it is a time of curious change.